Intro to Private Market Investments

- Disclaimer:

- Prepared by a Hobbyist Investor

- This presentation is created for educational purposes only and comes with no guarantees regarding its accuracy, completeness, or applicability for specific purposes. The content here should not be interpreted as any form of financial, investment, or trading guidance. Prior to making investment decisions, it's crucial to conduct your own research and seek advice from professional financial consultants.

- High Risk: Potential for Total Loss of Investment

- Prospects for financial returns in the short term (5-10 years) are minimal.

- Investing in the private sector demands a significant time commitment, often requiring 10 to 18 hours weekly, especially in the initial stages of investment.

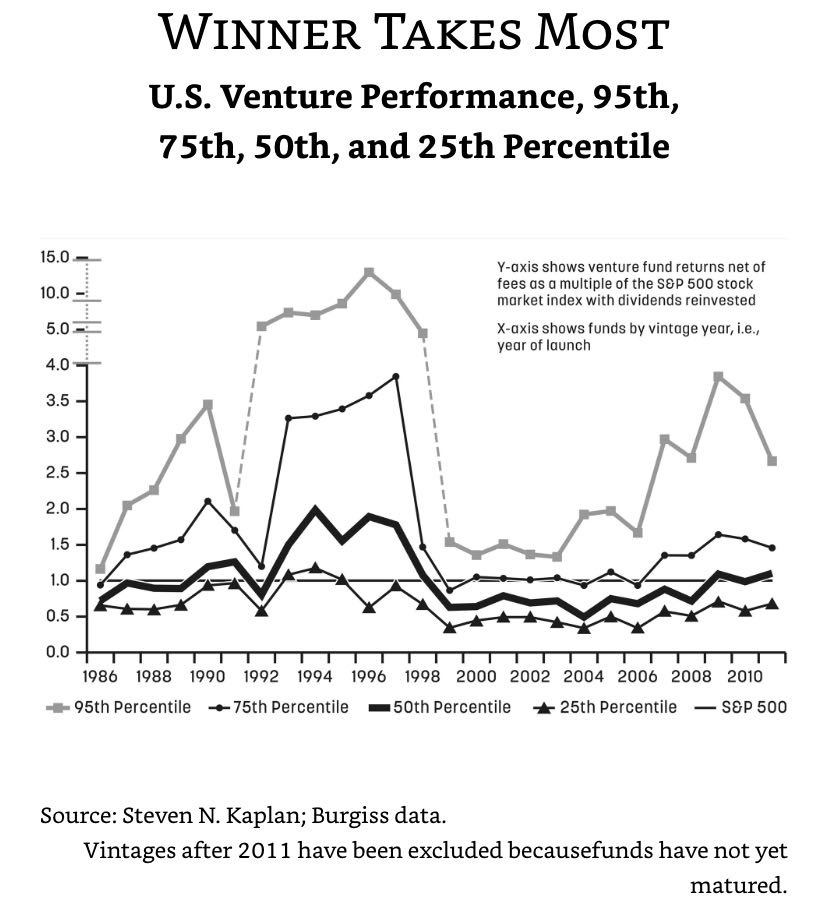

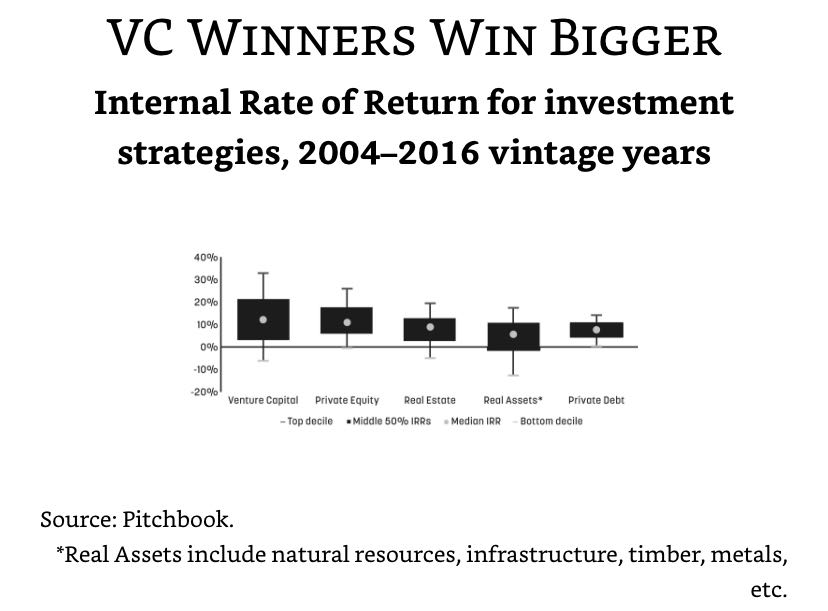

Why Private Market Investing: Return

S&P500's performance outruns p50 VCs from 2020 to 2010. And we need to be better than p75 to outrun S&P500.

| Winner takes most. | VC winners win bigger. (source) |

|---|---|

|  |

Why Private Market Investing: Opportunity

- Startups typically have extended durations in the private sector.

- The most rapid expansion phase for startups occurs while they are still privately held.

- This type of investment is oriented towards long-term value, offering reduced volatility compared to public markets.

- Major institutional investors, like Tiger Global and Coatue, are increasingly channeling funds into the private market.

Why Private Market Investing: Impact of Public Market Downturn

- The earlier the stage is, the less impact from public market.

- pre-IPO round will be heavily impacted.

- Example, Stripe was traded at $200B valuation in the secondary market with $650B annualized TPV in 2021. Paypal was used as the benchmark. Now Paypal(down 60% in the last 6 months) is trading at $120B market cap with $1.25T TPV. I believe Stripe should be valued between $65B~$95B

- Might be hard for VC to raise new fund but no impact to the existing funds raised in the last few years.

- Example, Tiger Global just raised the PIP 15 fund of $11B for series A&B investment.

- VC will be very likely to use public market as the benchmark to “lowball” the valuation of startups when negotiating term sheets.

Why Private Market Investing: Tax Benefit

- QSBS, applies only for early stage investment under certain criterias.

- Exclusion is for gains of $10M or 10X of your original investment.

- $25K Investment Pays $0 Federal Income Tax up to $10M Gain

- $2M Investment Pays $0 Federal Income Tax Up to $22M

- Capital Loss

- Under Section 1244 of the Internal Revenue Code, an ordinary loss deduction for a loss on stock from a “qualified small business corporation” can offset ordinary income and any capital gains. You can deduct up to $100,000 of losses from Section 1244 stock in any one year if married and file a joint return, or $50,000 if you file as single.

Why Private Market Investing: Career

- Build connections with founders, angel investors, venture capitalists. Be part of the community.

- Evaluate an opportunity of joining a startup.

- (For Angel Investor)Satisfaction that comes with being a Mentor / Therapist / Coach / Giver of tough love.

- Practice your product and engineering skills.

- Stay current and keep learning: Web3/SpaceTech/BioTech/Longevity/CleanTech etc.

- “It’s like a Free MBA Program.” - Lily Zhang, Senior Director of Instacart.

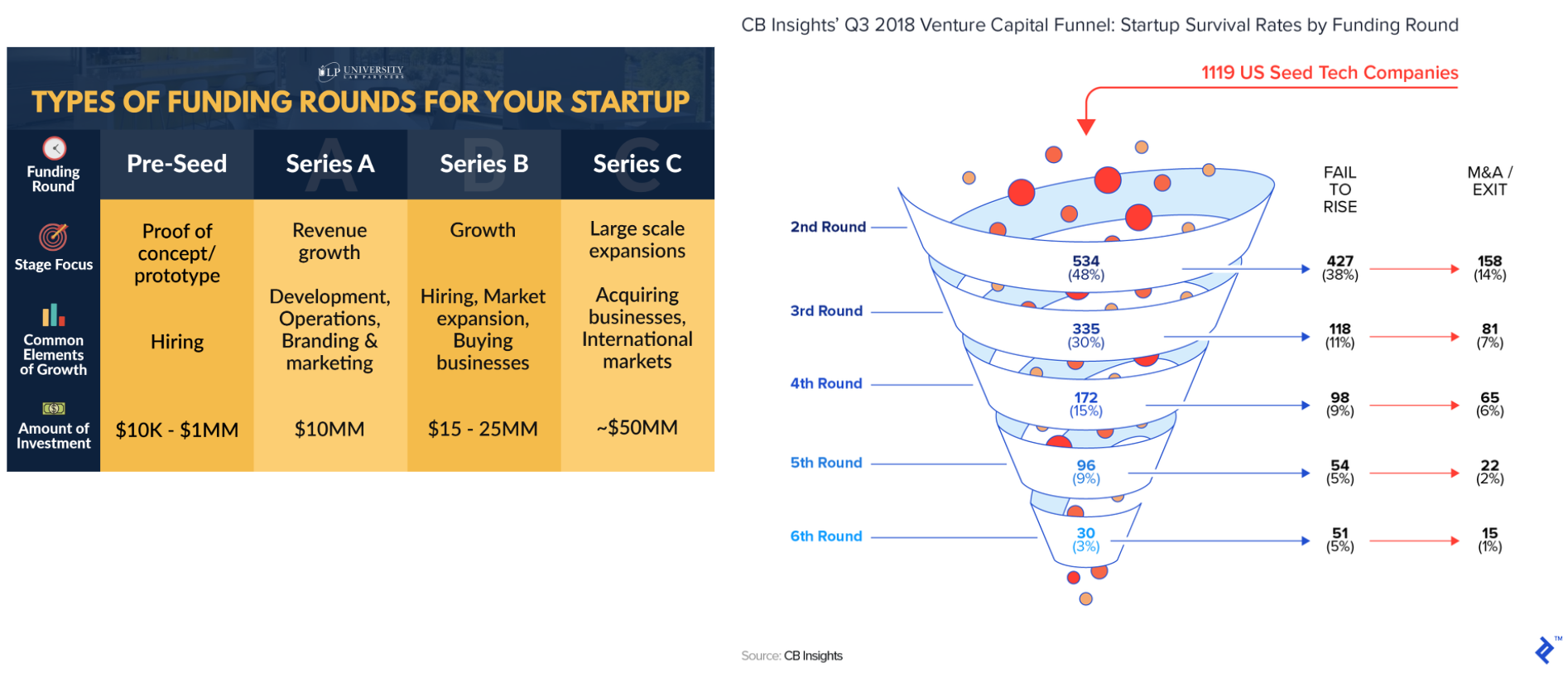

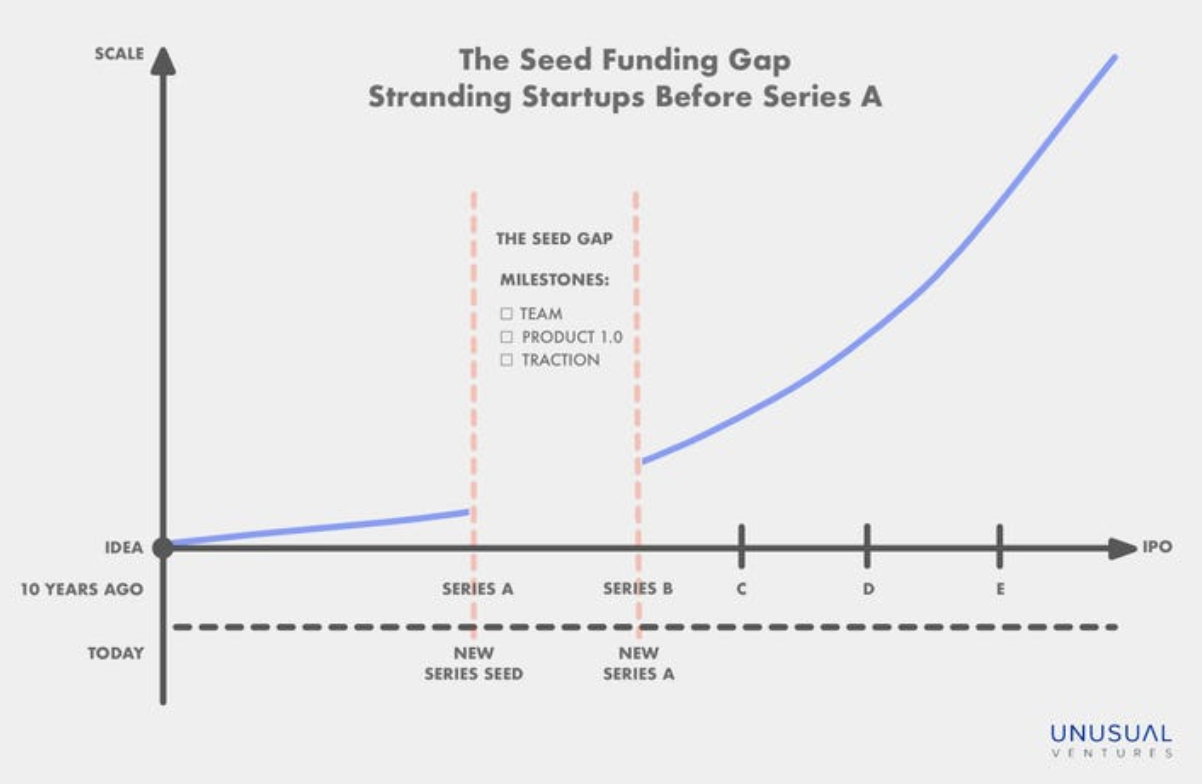

Investment 101: Fundraising

Fundraising Chasm

Investment 101: Terms

- Simple Agreement for Future Equity (SAFE)

- Cap and Discount

- Does not accrue interest

- Does not define a term for payback

- YC General Counsel answering a question regarding SAFEs

- Ambiguous fiduciary responsibility

- TopTal TWiST Episode

- Be Wary Of Uncapped SAFE Note!

- Convertible Note - provides for above

- Common Stock, Preferred Stock

- Pre-Money VS Post-Money

Investment 101: Cap Table

To calculate your ownership percentage and share price before and after the closing of each round is super complex. Here is a practice tool you can try, kudos to David Beaty, the founder of Gaingels.

Investment 101: Exit

- IPO

- M&A

- SPAC

- Direct Listing(Coinbase, Amplitude)

- Secondary Share Sale

- Dead Or Zombie

Investment Thesis: Basis

- Quick Filters

- Geography

- Sector(SAAS/Ecommerce/Fintech/Social/Delivery/SpaceTech…)

- Stage

- Typical micro VC funnel: 4K decks -> 400 meetings->20~40 investment. I reviewed almost 3K decks so far.

- Risks

- Execution. Vision & Roadmap & Speed.

- Eg, ARK7, an early entrant of fractional property share marketplace, was outpaced by many new entrants in the last two years due to its slow execution speed.

- Market.

- Eg, HRTech SAAS(Mocha, 北森 etc.) in China, Dentist Clinical SAAS in US/CA

- Technology

- SpaceX, Grail

- Team

- TeamOps which was endorsed by Bain Capital GP. CTO was kicked out of the company

- Regulation

- Crypto in China, Binance moved their HQ out of China.

- Financial. Burn rate, market dynamics.

- Katerra, SandboxVR

Investment Thesis: Trade Off of Early Stage Vs Late Stage

- The later the stage is, the less efforts and time needed as less due diligence efforts and post-investment follow ups.

- The later the stage is, the less risk and less return per deal.

Investment Thesis: Build Your Portfolio

Portfolio Strategy: Depth vs Breadth

Go Deep: Invest into a few, join the board and keep following on the future round. Eg. Mighty Capital

Go Wide: Widely spread the capital into many early stage companies. Rarely take the pro-rata. Eg, Ulu Ventures, GFC, FJ Labs, Uphonest etc.

Deep & Wide: VCs with large AUM. Eg, Accel, Khosla, A16Z

Power Law Is Real: Your overall return will be from a few mega winners. And most of your portfolio will have 0 return or mediocre return.

- “A few companies will generate most of your returns; the power law has been super-real for me. One company represents 85% of my gains, and the top 10 represent 95% of my gains (though most of my investments are early from the past 1-2 years).” —Daniel Rumennik, GP at AirAngels

Try it out to see how much overall return it can give to your portfolio if one of them has 1000X return: launch.co/model

Deal Sourcing: The Most Critical Part

- Access is way more important than picking.

- “As an angel investor, it’s more important to be swimming in a pool of good potential investments than to be an exceptionally good picker. Obviously if you’re able to be both, it’s better :) but if you had to choose between being in a position to see great deals and then picking randomly, or coming across average deals and picking expertly, choose the former.” —Jack Altman, investor and CEO of Lattice

- “VCs like to pretend that they’re really smart, but ultimately it’s just math. A single 100x or 1,000x deal will return your fund. But it’s nearly impossible to know which deal that will be. The important thing is to invest in enough deals that could 100x+.” —Julia Lipton, investor

- Golden Rule of verifying the deal flow quality: whenever you see a big fundraising round or great exit, to ask yourself—did I have a chance to invest in that company?

Deal Sourcing: How to Get Access to The Great Deals

- Accelerator Demo Day: YC, Xgoogler,StartX, Alchemist, TechStars, 500 Startups etc.

- Friend & Colleague

- Founders Community, events & conference.

- Other Investors, the most reliable channel

- Co-invest opportunity as LP of VC Fund

- Syndicates

- Inbound(Linkedin & Twitter), lowest quality

- Scouts network

- Cold Outreach Emails/DMs, way easier than I expected.

Deal Sourcing: recommended Syndicates

Happy to make a introduction except AirAngel :)

- The Syndicate. GP: Jason Calacanis

- Gaingels. GP: David Beaty, Paul Grossinger, Lorenzo Thione

- Stonks. GP: Ali Moiz, John Hancock

The Syndicates below are on Angellist:

- Uber Alumni or Moving Capital. GP: Amr Alshihabi

- Iterative Venture(FB Alumni). GP: Richard Chen

- DoorDash Alumni. GP: Bernard Liang

- Calm Venture. GP: Zachary Ginsburg

- AirAngel(Airbnb Alumni). GP: Lenny Rachitsky

- PlanB Venture. GP: Han Hua(Google Venture)

- MatchA. GP: Lily Zhang(Instacart, 领航), Lake Dai(LDV Venture Partner, employees#84 of Alibaba), Leo Liang(Coinbase)

- MyAsia. GP: Sajid Rahman

- Fox Venture. GP: Chad Fox

Deal Evaluation: Pre-SEED & SEED

- PMF(Product Market Fit). Would the customers be very disappointed without your product?

- Business Model. Demonstrated to be scalable, reasonable or high margin.

- Vision & Exit Strategy. Long term vision, ambitious to be a $10B or $100B business. Not dependent on M&A to exit.

- GTM Strategy. The execution/milestone in the next 18 months. User acquisition and growth channel.

- Competition. Is the value proposition unique? Can it be the category leader in this region? Is there an inherent operational advantage for local player vs global?

- Team. Founder market fit? Vibes among Co-founders. 1st time founder?(Not preferable unless emerging market such as Web3). Can they attract the best talents to achieve the vision?

- Co-Investor.

- Although top tier VC leading/joining the round is a very positive signal at most of the time, please be cautious about these VCs who just pour money blindly/aggressively:

- Tiger Global

- “Tiger Global’s investment strategy is to preempt companies six months prior to their planned fundraise, pick the best company in the space, and project their future valuation and offer a slight discount. This is a brilliant strategy because it prevents other preeminent venture firms (A16Z, Sequoia, etc…) from offering competing term sheets and further increasing the valuation” - From Somewhere

- A16Z, Coatue, Softbank, Insights Partner

- Tiger Global

- Although top tier VC leading/joining the round is a very positive signal at most of the time, please be cautious about these VCs who just pour money blindly/aggressively:

- “Most great ideas have been tried” - Mike Vernal, GP of Sequoia Capital

- “Competition is more about execution and growth traction.” - Cindy B, GP of CapitalX

- Don’t invest just because you really love the product.

Deal Evaluation: Growth Stage(Series A-C)

- TAM(Total Addressable Market). Need to be at least $1B. Bottom Up Estimation: # of customers * ARPU

- Traction. Growth rate (My threshold YoY >= 50%, strong conviction if MoM >= 10%) and Scalability.

- GTM Strategy: Sales led(Zoom/Rippling)/Marketing led(Snowflake)/Product led(Airtable/Notion)

- “We love either companies with large ACV or extremely large user base” - anonymized from Sequoia Capital

- Reasonable valuation? Can be compromised if it’s a rocketship.

- Co-Investor.Same as the previous slide.

- Competition: enough growth room to be a multi-billion company

- Upside: 10X+ return?

Deal Evaluation: Pre-IPO Stage

- Only One Factor: Upside

- I only take the opportunity with 10X+ multiples.

Due Diligence

- App Store

- Redflag: Release app version once a month

- Glassdoor

- Redflag: “Customers are confused about our product; Leadership has too many focus; Customer onboarding is not scalable…”

- Customer Testimony: ToB: call, G2; ToC: Reddit, Youtube, Amazon, App Store, App Annie.

- Redflag: Leads != Contracts. Over-exaggerated DAU/MAU.

- Linkedin

- Redflag: part time co-founder

- Financial Data. Tax return and bank statements.

- Redflag: Using booked ARR as realized ARR in pitch deck

- Founder background check

- Redflag: Criminal record of financial fraud(Bitnob); Founders/Advisors had no related experience in this domain(Theranos)

Value Add

- Be someone founders want to be on their cap table.

- Don’t underestimate your values to the founders

- Knowledge. Product, Growth, Marketing, Engineering, insights of a specific domain(eg, music, Web3, Biotech, Battery etc.)

- Hiring. “If you help a founder find and hire an engineer, as an example, you’re already in the top 0.01% of investors for them in terms of value-add.” —Charley Ma, investor and GM at Alloy

- Fund Raising. Time to “monetize” your investor networks

- Customer Access. Introduce customers.

- “Now there are two gold bars placed here, you tell me which one is noble and which one is sordid.”

- “The best way to maximize your return is to help the startups to be successful.” - SC Moatti, GP of Mighty Capital